In February 2025, the Chronic Disease Flexible Coverage Act (H.R. 3800) was introduced in the House of Representatives. The bipartisan bill would codify IRS Notice 2019-45, which expands the safe harbor of HSA-HDHPs to cover 14 specific chronic disease services and items on a pre-deductible basis, and would allow the list of services to be expanded if necessary. IRS Notice 2024-75 has included 4 additional items to be covered prior to meeting the plan deductible.

Health Savings Account-eligible high-deductible health plans (HSA-HDHPs), which provide a tax-free savings account paired with an HDHP, represent a growing percentage of plans offered on the individual and group market. As of 2017, 43% of Americans were enrolled in plans with high deductibles, which represents a nearly threefold increase from 2007. Enrollment is higher for private sector employees, at 53% in 2022. Employers are increasingly offering HSA-HDHPs to expand coverage options, lower their health care spending, and promote proactive customer engagement. However, in these plans, enrollees with chronic conditions are required to pay out-of-pocket for necessary services prior to meeting the plan deductible, resulting in lower utilization of care, poorer health outcomes, and higher costs. Expanding coverage of preventive care would lead to improvements in health equity, as individuals harmed by high deductibles are often financially insecure, Black and Brown populations, and have chronic conditions.

Congressional Efforts to Expand Pre-Deductible Coverage

In response to Executive Order 13877, the U.S. Department of Treasury issued Notice 2019-45 in July 2019. IRS Notice 2019-45 allows HSA-HDHP plans the flexibility to cover 14 specified medication and services used to treat chronic diseases prior to meeting the plan deductible. In October 2024, IRS Notice 2024-75 added 4 additional items to the list of services covered pre-deductible. A previous guidance from the IRS allowed HSA-eligible HDHPs the ability to provide select preventive care benefits prior to satisfaction of the plan deductible, but services and medications used to treat chronic conditions were excluded. Primary prevention, while important, is a small component of overall health spending. By contrast, spending on chronic disease encompasses nearly 90% of total U.S. health care expenditures.

With these policies in place, all high-deductible plans are now able to adopt a more flexible benefit design offering more protection for certain medical services through a value-based insurance design plan structure. 64% of HDHP enrollees have indicated that they would likely select an HDHP if it covered preventive care for chronic conditions before the deductible was reached, and employers recommend prioritizing coverage of preventive care medication pre-deductible as fully as HSA federal regulations allow.

Table: Chronic Disease Management Services in the Expanded Safe Harbor of IRS Notice 2019-45 and IRS Notice 2024-75*

| Preventive Care Service | For Individuals Diagnosed With |

|---|---|

|

Angiotensin Converting Enzyme (ACE) inhibitors |

Congestive heart failure, diabetes, and/or coronary artery disease |

|

Anti-resorptive therapy |

Osteoporosis and/or osteopenia |

|

Beta-blockers |

Congestive heart failure and/or coronary artery disease |

|

Blood pressure monitor |

Hypertension |

|

Inhaled corticosteroids |

Asthma |

|

Insulin and other glucose lowering agents |

Diabetes |

|

Retinopathy screening |

Diabetes |

|

Peak flow meter |

Asthma |

|

Glucometer |

Diabetes |

|

Hemoglobin A1c testing |

Diabetes |

|

International Normalized Ratio (INR) testing |

Liver disease and/or bleeding disorders |

|

Low-density Lipoprotein (LDL) testing |

Heart disease |

|

Selective Serotonin Reuptake Inhibitors (SSRIs) |

Depression |

|

Statins |

Heart disease and/or diabetes |

|

Oral Contraception* |

|

|

Male Condoms* |

|

|

Breast cancer screening* |

|

|

Continuous glucose monitors and Insulin* |

|

Building on momentum of Executive Order 13877 and IRS Notice 2019-45, the Chronic Disease Flexible Coverage Act (H.R. 3800) was introduced in the House of Representatives by Vern Buchanan (R-FL) and Jimmy Panetta (D-CA) in February 2025. The act would further establish the flexibility of pre-deductible coverage of specific chronic care services and medications included in IRS Notice 2019-45 by codifying the guidance. The bill previously passed in the House of Representatives on September 17, 2024 (during the 118th Congress).

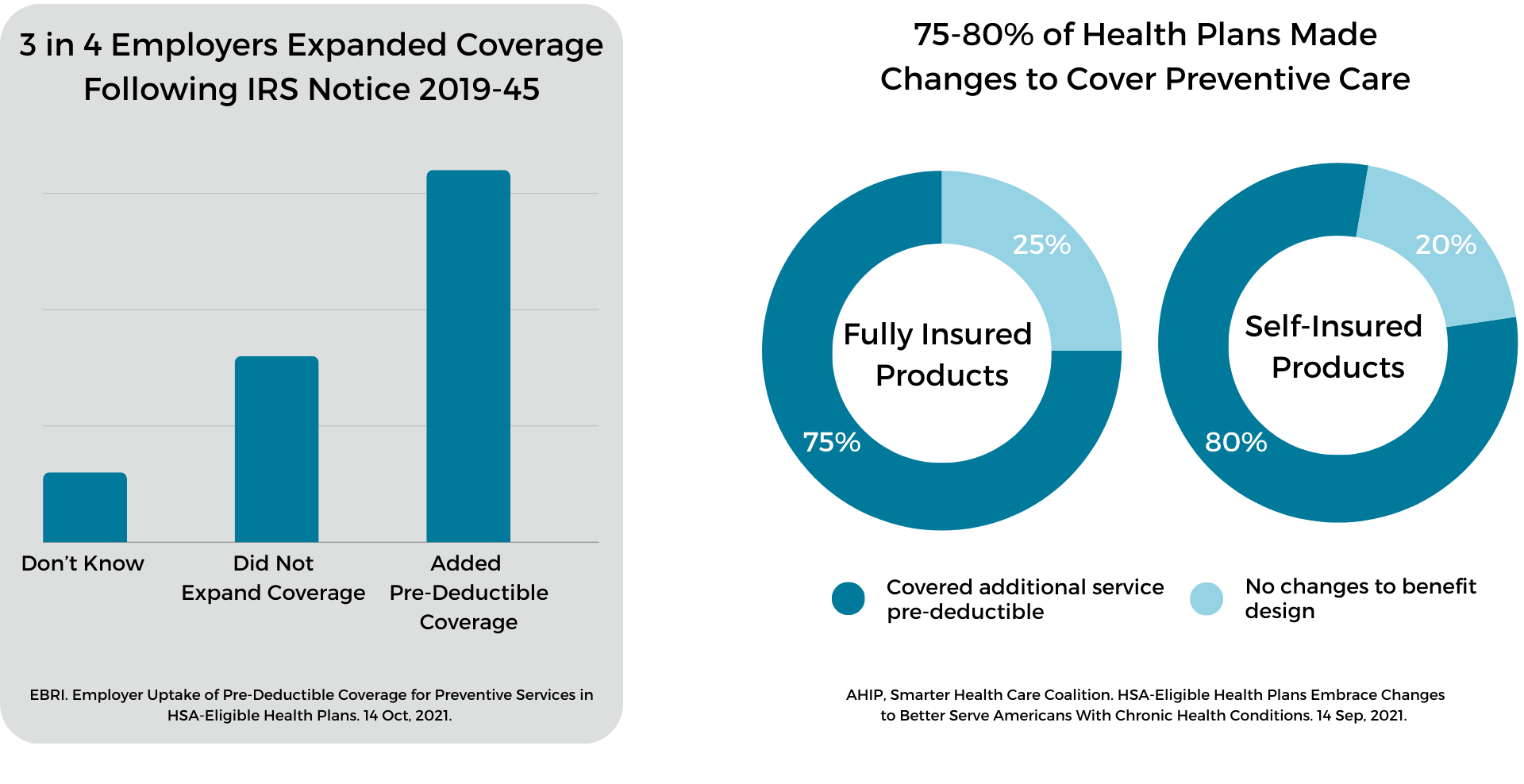

Research from EBRI shows that following the passage of IRS Notice 2019-45, 76% of employers and 75-80% of HSA-eligible plans made changes to cover new chronic disease preventive services pre-deductible. Expanding pre-deductible coverage of HSA-eligible health plans had little impact on premiums, increased use of preventive care, and increased medication adherence. Although there is no overall spending difference between PPOs and HSAs, HSA enrollees use outpatient services less, fill prescriptions less, and use inpatient services more than PPO enrollees.

Smarter Deductibles, Better Value: Expanding Coverage in HSA-HDHPs

81% of employers indicated that they would add pre-deductible coverage for additional healthcare services if allowed by law, and congressional efforts to further expand the list of chronic care services covered pre-deductible are already underway.

The Chronic Disease Management Act was introduced in the Senate (S. 1948) and the House of Representatives (H.R. 3709) in 2019. This bipartisan, bicameral legislation would codify IRS Guidance 2019-45 and provide high-deductible health plans the flexibility to provide coverage for services that manage chronic diseases prior to meeting the plan deductible. The bill was reintroduced year-over-year until 2021.

81% of employers indicated that they would add pre-deductible coverage for additional healthcare services if allowed by law

The CARES Act, signed into law in March 2020, allowed HSA-HDHPs to cover all telehealth on a pre-deductible basis. Telehealth services benefit seniors, those in rural areas, and those with chronic conditions by offering frequent, low-barrier check-ins. To make this pre-deductible benefit permanent, the bipartisan, bicameral Telehealth Expansion Act (H.R. 1843) and the Preserving Telehealth, Hospital and Ambulance Access Act (H.R. 8261) were introduced in the House of Representatives in March 2023 and May 2024, respectively. Both bills were passed by the House Ways and Means Committee.

As the market for HSA-eligible HDHPs grows, it is important that these plans use this flexibility to allow for effective health management for all beneficiaries. A targeted strategy exploring coverage for certain high-value, clinically-indicated health services prior to meeting the deductible will produce more effective clinically-nuanced designs without fundamentally altering the original intent and spirit of these plans. Adoption of voluntary, clinically-nuanced expanded HDHP benefit designs has the potential to mitigate cost-related non-adherence, enhance patient-centered outcomes, allow for lower premiums than most PPOs and HMOs, and substantially reduce aggregate health care costs expenditures.